Saint John, New Brunswick (Canva)

Don’t miss out—join us online for REM’s first monthly market breakdown for Realtors on Feb. 25 at 2 PM Eastern. Hosted by REM, columnist Daniel Foch will dive into CREA’s latest stats and key market trends. Have questions? Leave them in the comments or send them in advance to editor@realestatemagazine.ca. Register here.

Something has shifted in Canada’s housing market. This shouldn’t come as a surprise, given something has certainly shifted at a global geopolitically level. You might even call it a “tarrifying” headwind for Canada’s real estate market.

For years, supply was tight, and homebuyers outnumbered sellers in Canada’s real estate market. But as 2025 begins, the landscape looks strikingly different. New listings are pouring into the market at an extraordinary pace, while sales are faltering under the weight of mounting economic uncertainty.

As is tradition, when facing an unknown future, Canada’s real estate market has decided to hit the “pause button.” It is not uncommon to see the market take a breath when we’re facing a historic election, a pandemic or a changing economy. Today’s trade war is no different.

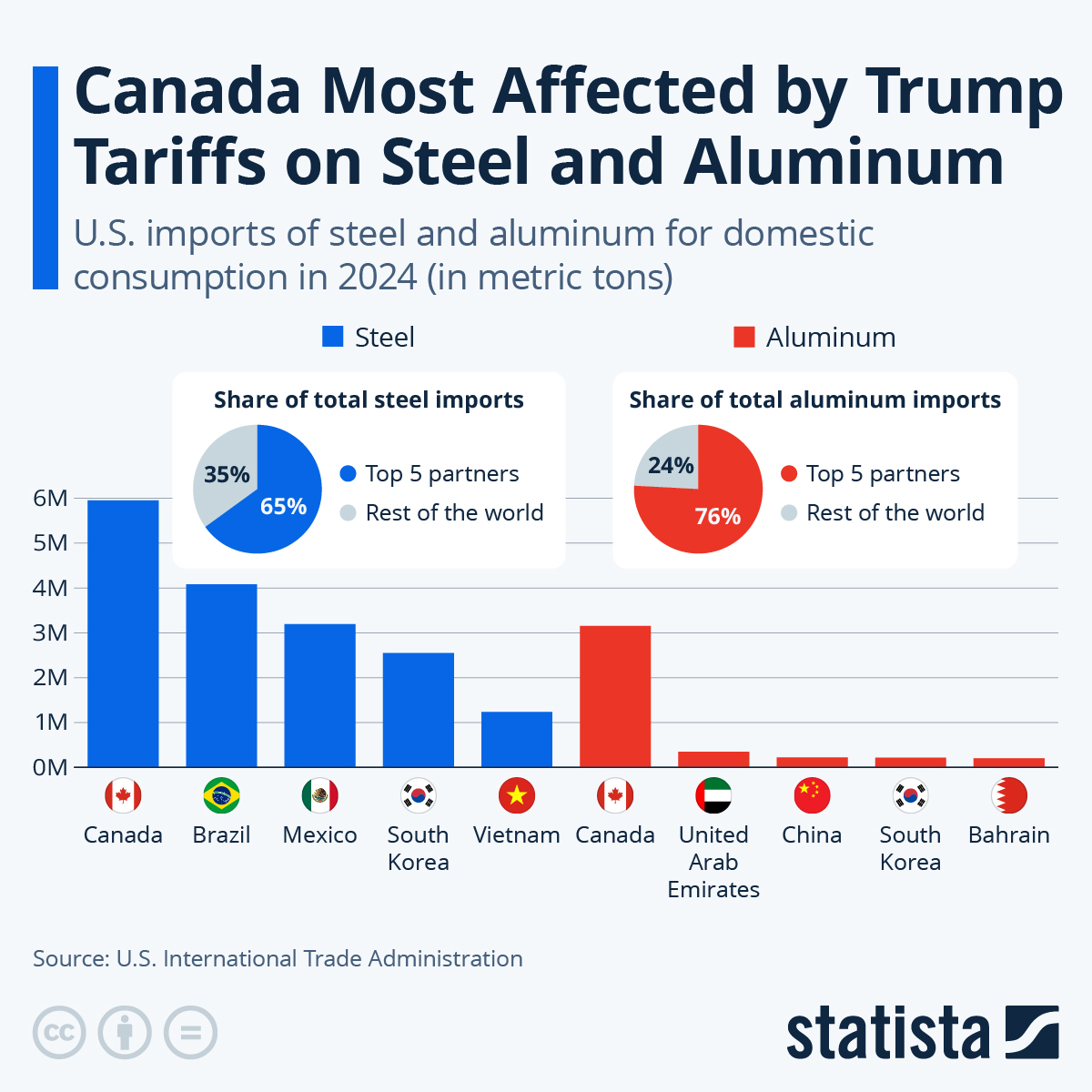

Compounding the turbulence, President Trump’s proposed tariffs on Canadian exports loom over key industries, raising concerns about potential job losses, wage stagnation, and the broader impact on housing demand. Though the Canadian-specific targeting has been temporarily postponed, Trump’s global target on steel and aluminum has Canada written all over it.

A historic surge in listings, a slowdown in sales

For buyers willing to stomach the risk, this could be the window of opportunity they’ve been waiting for—more choices and lower interest rates make financing more attractive. But for sellers, it’s a wake-up call. A market that once favoured them is now shifting toward balance—or even softness in some areas. Yet, the full impact of these shifting dynamics remains uncertain, as much depends on the outcome of the postponed tariffs and their potential ripple effects across the economy.

CREA’s January market data gives us a clearer picture of what’s ahead. Let’s break it down.

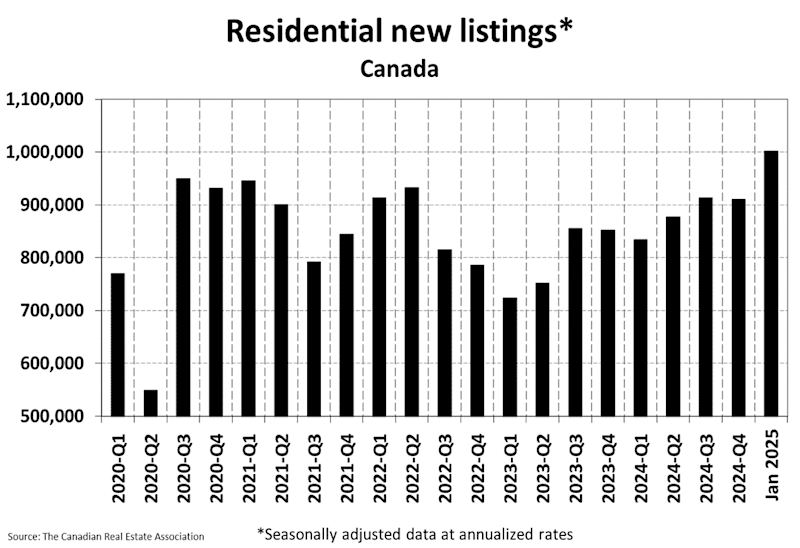

Unprecedented inventory growth

One of the biggest surprises of early 2025 has been the flood of new listings. Figures for January reveal that new supply jumped 11 per cent compared to December 2024—the largest seasonally adjusted increase since the late 1980s (excluding pandemic-era fluctuations).

What does this mean? It’s a clear sign that more homeowners are choosing to sell, possibly in anticipation of weaker market conditions. In high-priced regions like British Columbia and Ontario, where supply had been tightening in 2024, this sudden increase in listings is cooling price pressures and shifting negotiating power back toward buyers.

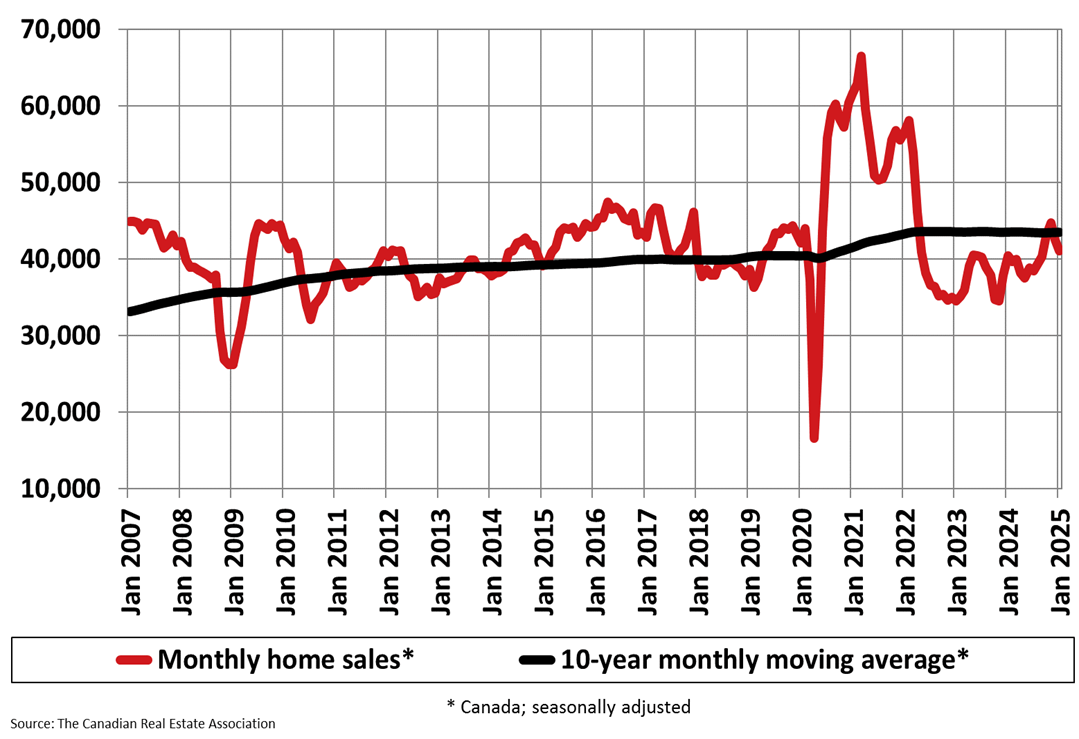

Sales take a hit amid economic jitters

While inventory rose, sales did not follow suit. Instead, national home sales fell 3.3 per cent month-over-month, with the most dramatic drop occurring in the last week of January. The timing suggests that buyers pulled back due to growing concerns over Trump’s tariff policies, which many fear could destabilize Canada’s economy.

However, it’s not all bad news. Compared to January 2024, actual sales were up 2.9 per cent, meaning demand is still present—just hesitant. Buyers aren’t disappearing, but they are waiting to see where the economy lands before making big moves.

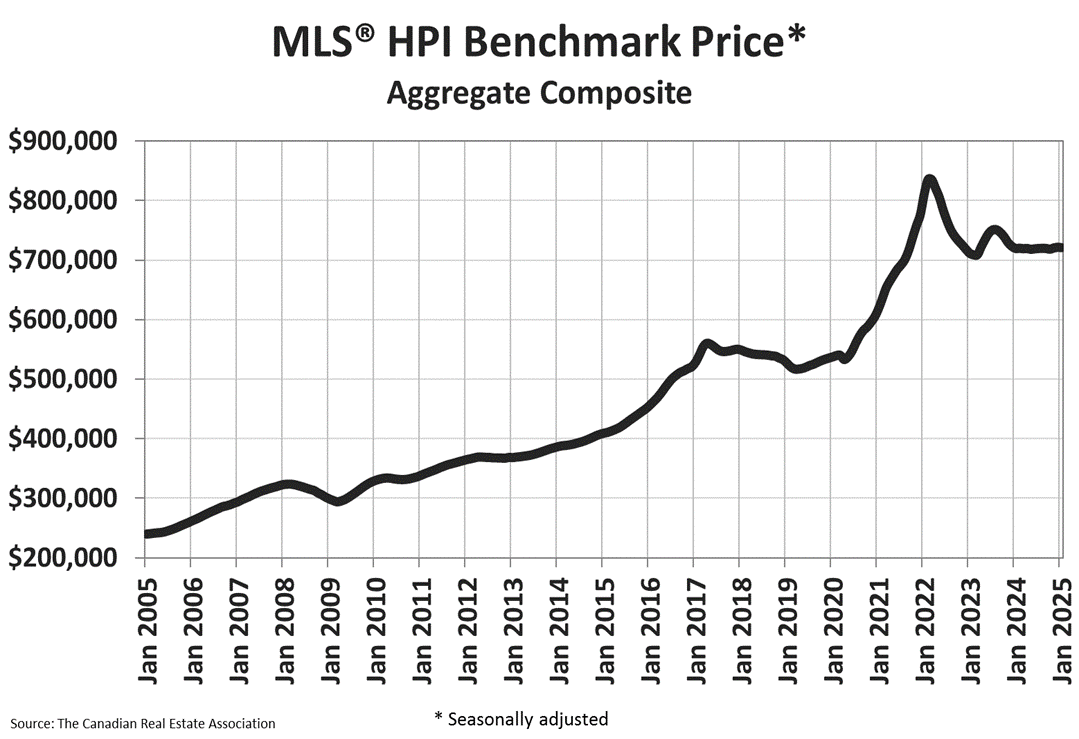

Prices hold their ground—for now

Despite rising inventory and weaker sales, home prices have remained surprisingly stable:

- The MLS Home Price Index (HPI) barely changed month-over-month (-0.08 per cent) and year-over-year (+0.07 per cent).

- The national average home price hit $670,064, up 1.1 per cent from January 2024.

But not all regions are experiencing the same trends:

- British Columbia and Ontario: A surge in supply is creating a softer pricing environment, making these regions more favourable for buyers.

- Alberta and Saskatchewan: With inventories at near 20-year lows, prices continue to rise despite economic uncertainty.

- Quebec and Atlantic Canada: These markets are expected to see both price and sales growth in 2025, making them the country’s most balanced housing sectors.

The big unknown

A game-changer for the Canadian economy

Just as Canada’s housing market was poised for recovery, a new storm appeared on the horizon: Trump’s tariff policy for Canada.

The U.S. government has proposed a 25 per cent tariff on all Canadian non-energy exports and a 10 per cent tariff on Canadian energy exports, though implementation has been postponed by 30 days. If implemented, this policy shift could disrupt key industries, hamper trade and increase the risk of an economic downturn.

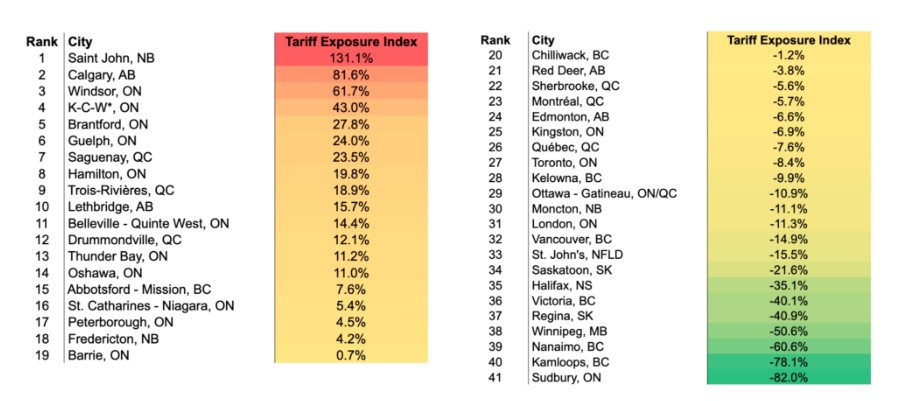

Some cities will feel the effects more than others. New research from the Canadian Chamber of Commerce’s Business Data Lab has identified the regions most vulnerable to these tariffs. The most exposed markets are:

- Saint John: Due to its heavy dependence on crude oil exports from the Irving Oil Refinery.

- Calgary: A major energy hub exporting crude oil, natural gas, and beef.

- Southwestern Ontario (Windsor, Kitchener-Cambridge-Waterloo, Brantford, Guelph): These cities are deeply tied to the auto and manufacturing industries, which rely heavily on cross-border trade with the U.S.

- Hamilton, Ontario: As Canada’s steel capital, Hamilton’s economy is at risk if tariffs disrupt steel exports.

- Quebec’s aluminum and forestry hubs (Saguenay, Trois-Rivieres, Drummondville): Key exporters of aluminum and forestry products.

If these industries slow down, it could impact jobs, wages, and housing demand in these cities. Simply put, these tariffs could mean fewer buyers in affected regions, leading to longer selling times and price stagnation or declines.

The table below, from the same research, provides a detailed ranking of Canadian cities most vulnerable to the proposed U.S. tariffs.

What’s next?

The spring rebound is coming—but will it be enough?

Despite economic concerns, CREA still expects a strong spring market, driven by lower borrowing costs (mortgage rates are falling, drawing more buyers into the market) and pent-up demand (many buyers have been waiting for prices to stabilize before re-entering).

According to CREA, an estimated 532,704 homes will sell in 2025, an 8.6 per cent increase from 2024. Prices are expected to rise 4.7 per cent this year, reaching $722,221 by year-end.

Not every market will recover equally

- British Columbia & Ontario: Sales should rebound, but higher inventory will keep prices in check.

- Alberta & Saskatchewan: With sales already near record highs in 2024 and inventory at 20-year lows, prices in these provinces are expected to climb faster than sales.

- Quebec & Atlantic Canada: Predicted to see both price and sales growth.

What Realtors need to consider

For buyers

- More listings, more choices – Buyers finally have leverage in many regions.

- Lock in rates now – Mortgage rates are dropping, and delaying could cost more in the long run.

- Watch the economy – If tariffs cause widespread job losses, it could create a buyer’s market later in the year.

For sellers

- More competition means smarter pricing – Overpricing will lead to stagnation, especially in high-inventory regions.

- Consider selling before a potential slowdown – If economic fears grow, waiting could mean a tougher market.

- Regional differences matter – Some markets (like Alberta) still favour sellers, while others (Ontario) are shifting toward buyers.

Final thoughts: A market on the edge

The Canadian housing market in 2025 is no longer a one-way street. Buyers and sellers must adapt to new realities, from shifting supply-demand dynamics to the potential fallout of a major trade war.

For some, this year will bring opportunity; for others, waiting may be the preferred choice.

How the market unfolds will depend on a delicate balance of forces—interest rates, inventory levels, and the broader economic impact of U.S. trade policies. While the housing sector has shown resilience before, this time, the uncertainty runs deeper, and its effects may take longer to play out.

Don’t miss out—join us online for REM’s first monthly market breakdown for Realtors on Feb. 25 at 2 PM Eastern. Hosted by REM, columnist Daniel Foch will dive into CREA’s latest stats and key market trends. Have questions? Leave them in the comments or send them in advance to editor@realestatemagazine.ca. Register here.

Daniel Foch is the Chief Real Estate Officer at Valery.ca, and Host of Canada’s #1 real estate podcast. As co-founder of The Habistat, the onboard data science platform for TRREB & Proptx, he helped the real estate industry to become more transparent, using real-time housing market data to inform decision making for key stakeholders. With over 15 years of experience in the real estate industry, Daniel has advised a broad spectrum of real estate market participants, from 3 levels of government to some of Canada’s largest developers.

Daniel is a trusted voice in the Canadian real estate market, regularly contributing to media outlets such as The Wall Street Journal, CBC, Bloomberg, and The Globe and Mail. His expertise and balanced insights have earned him a dedicated audience of over 100,000 real estate investors across multiple social media platforms, where he shares primary research and market analysis.

If what buyers want is quality-built (like 15-20 yr ago) home on decent lot (50 x 100) at $650K (if interest rates are 5-6%)

And

What sellers are offering is a 2yr old poorly-built condo/townhouse (or 55 yr old detached with lots to do) and expecting a million or better ….

it’s no wonder we have a housing problem (mischaracterized as ‘Affordability Crisis’).

No amount of gov’t-subsidized, market-rent, hi-rise Rentals nor on-the-transit-line condos will solve this.

If Global-Weather-caused-by-Carbon& Cars is a false demon then we can free up the Greenbelt OR (in the interim) build satellite-cities n/w and n/e of GTA to supply what buyers want at prices they can afford.

Values have changed. How can you say they remain steady? With the number of sales on a downward trend values will follow. What is skewing values is that many seller’s may be underwater and cannot sell below a certain price. So the properties sit on the market. And the banks, not wanting to go power of sale, work with the home owners to keep them in their homes. This charade cannot go on forever. It has been going on for over two years now. If home owners begin to lose jobs as the economy weakens then it will be nothing but disaster. I read about colleges laying off staff, the auto industry, steel industry and oil exports all in trouble. These facts will eventually hit the job markets. Once again a realtors point of view is a increase in spring activity, opportunity for buyers with lower interest rates. But with values high, lower interest rates will have little impact. I say fasten your seat belt, the plane flipping over was not an accident. It was an omen!