The Greater Toronto Area (GTA) housing market experienced a period of stability on a month-over-month basis in May, with home sales remaining at a low 7,013 transactions, the Toronto Regional Real Estate Board (TRREB) reports.

That being said, “stability” is not really what you want on a monthly basis in the middle of what ought to be a spring market. In a typical year, transactions rise pretty consistently from January until May. When looking at an annualized context, it’s a significant 21.7 per cent decline from the 8,960 sales in May 2023, so it’s no surprise that Ontario Real Estate Association (OREA) CEO, Tim Hudak, has publicly called for rate cuts.

Unaffordable markets see very little transaction volume — a problem for the industry

Hudak’s comments bring attention to something that is painfully apparent in advanced economies with lower homeownership than Canada: unaffordable markets see very little transaction volume.

While this is not necessarily a bad thing for consumers of housing, it’s certainly a bad thing for an industry that depends on transaction volume to make a living. This is why countries like Canada and the United States have large numbers of realtors per capita, whereas countries like Switzerland and the United Kingdom have very little.

Much of the transaction volume that professionals do see in these markets is in leasing, which has become a growing share of income for real estate professionals in the GTA during this record-low period of sales volume.

It has not been hard to find acknowledgment of Canada’s crippling housing affordability issue from economists at Canada’s biggest banks, for example, with RBC’s analysis:

People will start buying houses when they can afford to

From my perspective, in order to see meaningful growth in transaction volume, we need housing to be affordable again. It’s so simple that people call me stupid when I say it, yet it appears to be so easily ignored.

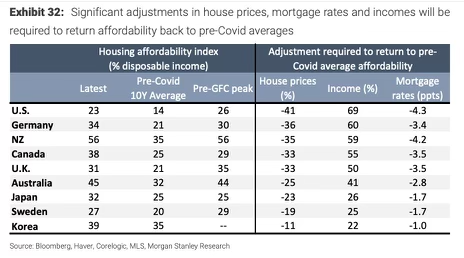

Bloomberg broke down what it would take for Canada to see a retreat from this affordability crisis:

- A 33 per cent decrease in house prices, and/or

- A 55 per cent increase in incomes, and/or

- A 350 basis point decrease in mortgage rates

The average selling price for homes in the GTA in May was $1,165,691, marking a 2.5 per cent decrease from May 2023’s average price of $1,195,409. Similarly, the MLS Home Price Index composite benchmark saw a year-over-year decline of 3.5 per cent.

Despite prevailing high interest rates, there was a modest month-over-month uptick in the average selling price on a seasonally adjusted basis from April 2024, indicating slight strength in the bid of buyers in today’s spring market.

“Inflation could be higher … if house prices in Canada rise faster than expected, or if wage growth remains high relative to productivity”

With this updated annual decrease in house prices, we have arrived at a juncture where prices continue to do the bulk of the work in restoring affordability. Measured from the peak of the market, house prices are down 20-30 per cent, depending on which metric and market you use.

Mortgage rates have only just begun to move down 25 basis points this week, and incomes have risen a nominal 2.5 per cent since 2022. Without further material changes in incomes or interest rates, it would not be unreasonable to expect house prices to continue bearing the burden of increased affordability, as fewer and fewer Canadians can afford to buy homes.

The Bank of Canada acknowledged this in their press conference opening statement for the June rate cut — by stating that “Inflation could be higher … if house prices in Canada rise faster than expected, or if wage growth remains high relative to productivity.”

As such, the Bank of Canada is a little bit stuck here when it comes to restoring housing affordability, as that growth in wages or house prices would decrease their likelihood of further cuts.

Reasonable to expect a buyer’s market this summer

Despite the annualized decrease in demand. new listings showed a contrasting trend, increasing by 21.1 per cent year-over-year to reach 18,612. The combination of the increased supply (listings) and decreased demand (sales) is sending us on an expedited path toward a buyer’s market, which is typically coupled with downward price discovery.

This influx of new listings provided prospective buyers with a larger range of choices and greater negotiating power, leading to a less competitive market environment compared to the previous year. The supply/demand imbalance led to a relatively low sales-to-new-listings ratio. Given supply growth alongside a typical summer decline in buying activity, it would be reasonable to expect a buyer’s market this summer.

While many are optimistic that interest rate cuts will be the beginning of the end for unaffordability and low-volume challenges in Canada’s real estate market, this reality comes at a cost. Much of the listing volume increase we see after rate cuts take place could come as a result of financial stress on borrowers, despite their slight relief.

Mortgage rate delinquencies rise after rate cuts

There are two reasons why mortgage delinquency rates typically rise after rate cuts take place:

- The lagging impact of rate hikes being felt on borrowers

- The reality that central banks cut rates in response to bad economic data, which leads to more bad data such as rising unemployment, which constricts household ability to service debt

This was well visualized by Ben Rabidoux of Edge Realty Analytics:

Caution, dangerous curves ahead

Currently, the housing market is characterized by cautious behavior among buyers, largely driven by high mortgage rates. According to Ipsos’ recent polling, a significant number of prospective homebuyers are holding off until they see concrete evidence of mortgage rates dropping. Even the Bank of Canada’s rate cuts may not accomplish that goal, given that the Canada five-year bond yield, the primary pricing mechanism for five-year fixed mortgage rates, just went up in response to June 7 data from the U.S.

It’s expected that as borrowing costs decrease over the next 18 months, a substantial number of buyers, including many first-time buyers, will be drawn into the market. This surge in demand is expected to ease some strain on the tight rental market, as these new homeowners transition from rental properties.

Jason Mercer, TRREB’s chief market analyst, pointed out that although high interest rates have tempered home prices, affordability will likely improve as borrowing costs decrease. However, this improvement may be short-lived as increasing demand is expected to exert upward pressure on home prices again.

Source: TRREB

Daniel Foch and Nick Hill are co-hosts of The Canadian Real Estate Investor Podcast. Daniel Foch, a real estate broker and analyst, is frequently featured in major media and has advised on over $1BN in real estate transactions, focusing on affordable housing. Nick Hill, a real estate investor and mortgage agent, has a background in business, commercial real estate and startups, working with investors and developers across Canada.

Exhibit 32 from Bloomberg cited as “Bloomberg broke down what it would take for Canada to see a retreat from this affordability crisis:”

I’m intrigued by the survey’s data

Can you recall the source issue etc