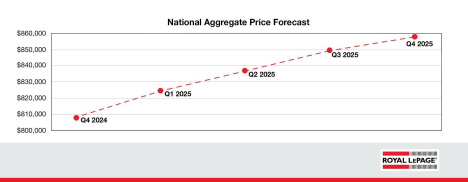

The Canadian housing market is poised for stability in 2025 as declining interest rates and new lending rules bring buyers back to the market, according to Royal LePage’s Market Survey Forecast. The company predicts the average price of a home in Canada will rise by 6 per cent year-over-year to $856,692 in the fourth quarter of 2025, falling in line with long-term trends.

Single-family detached homes are expected to see a 7 per cent price increase, reaching a median value of $900,833, while condo prices are forecasted to grow by 3.5 per cent, reaching $605,993. “The backlog of willing and able buyers continues to grow, and upcoming changes to mortgage lending rules will further enhance Canadians’ borrowing power,” says Phil Soper, president and CEO of Royal LePage.

The Bank of Canada’s recent monetary policy shift, from “inflation fighter” to “economy booster” has been a key driver of this optimism, Soper points out. “We saw a marked increase in market activity at the start of the fourth quarter, following the Bank of Canada’s 50-basis-point rate cut,” he notes, adding that buyers, for the most part, believe home prices have bottomed out.

Regional price trends will reflect strong demand

The forecast predicts price growth across all major Canadian markets, with Quebec City leading the way at an expected 11 per cent increase in the price. Edmonton and Regina follow with projected gains of 9 per cent each. Meanwhile, Greater Montreal is expected to see a 6 per cent increase, outpacing the Greater Toronto Area’s moderate 5 per cent gain and Metro Vancouver’s 4 per cent increase.

“Over the past several months, supply has been building in the Toronto and Vancouver real estate markets as sellers responded to early interest rate cuts by listing their homes. However, with home prices in these cities remaining high, many sidelined buyers continued to wait for more favourable borrowing conditions,” Soper explains.

“Flat property prices also reduced the urgency often driven by fears of ‘missing out,’ creating a temporary stalemate where inventory lingered, and buyers hesitated to act. By mid-fall, this dynamic began to shift as buyers re-engaged with the market.”

Expanded lending rules should help first-time buyers

New mortgage rules set to take effect Dec. 15, 2024, aim to provide greater access to housing for first-time buyers and those purchasing new construction homes. These changes include eligibility for 30-year amortizations on insured mortgages and an increase in the mortgage insurance cap from $1-million to $1.5-million.

“First-time buyers will be the primary beneficiaries of these initiatives, as their ability to borrow more for less with a smaller down payment will help bring them closer to their first home purchase,” said Soper. “We believe the return of buyers to the market will encourage builders and trigger a wave of new supply, which is very much needed.”

Policy and economic factors

There is the potential for disruptions from political changes both domestically and in the U.S. New housing policies following a federal election in Canada, along with the trade agenda of the incoming Trump administration in the U.S., could have ripple effects on Canada’s housing market, Soper flags.

Outlook for 2025

The strongest quarterly gains are forecast for the first quarter of 2025, driven by an early spring market. National home prices are projected to increase 2 per cent from Q4 2024 to Q1 2025, followed by more moderate gains of 1.5 per cent in the second and third quarters, and 1 per cent in the final quarter of the year.

Soper anticipates 2025 will bring a level of normalcy, “After several years of unusual volatility in the real estate market, key indicators point to a return to stability in 2025.”

Read Royal LePage’s full report, including regional highlights.

There was really no unusual volatility in the market the past two years. The market conditions were typical of an over heated sellers market for close to 24 months. The Globe and Mail reported this morning that the Jobless rates hits 6.8%. The highest since 2017 outside of the pandemic. How many first time buyer’s can afford a home of One Million to One and a Half Million? How are the current economic conditions going to support any increase in real estate values? And if values go up Canadians are in the same boat of affordability. The only job creations under Trudeau have been in the public sector. That is not a healthy economy. Mortgage applications are declining and economists predict this trend will continue into 2025. Not sure how that translates to a booming spring market. Prime Rate has nothing to do with mortgage rates. And there will most likely be an election early next year in Canada. A change of leadership will be disruptive to the housing markets. Buyer’s will not be jumping on the band wagon. And most prudent Canadians will wait it out to see how the Trump administration plays out before taking on a mountain of debt. In almost thirty years I have never once read a realtor perspective prediction that did not state a booming market, values increasing and a rosy for caste for the upcoming year. Its like the “Boy That Cried Wolf” . So I don’t know how much faith a consumer would put in these unsubstantiated predictions from realtors. I think a better prediction would be that 2025 will be an unpredictable volatile year for Canadians.

I agree with D O Realty. Where does Phil Soper get his information that homes will increase by 5%. Unemployment is high, mtge rates are high, a lot of mortgages are up for renewal in 2025, and a lot of people will not be able to afford the new payment, so they have to sell. There will be a lot of listing coming out in 2025. The buyers will know that seller are motivated to sell and they will low ball the offers and prices will come down just like the condo market is now.

The fact that prices have slowly increased overall for the past 2 years with SAME conditions and worse rates. Just because YOU cannot afford a home doesn’t mean that others can’t. All legislation is being shifted for people to borrow MORE, not LESS. New FHSA adding money for first home buyers, RRSP homebuyers plan increased to 60k per person, decreasing rates, people will have more money for housing than ever. Yes unemployment is rising but in case of recession, the governments will do exactly what they did when markets should’ve collapsed in 2020: support homebuyers and leave tenants out to dry. I’m not a real estate agent but just a young professional who accepts reality. The government will always support home ownership.

“commentary on housing market trends and data on price and forecast values are provided by Royal LePage residential real estate experts, based on their opinions and market knowledge”. So a survey of Royal LePage agents? 😮