Don’t miss out—join us online for REM’s monthly market breakdown on June 24 at 2 PM ET. REM, columnist Daniel Foch will analyze CREA’s latest stats, regional variations and what shifting sentiment means for Realtors—register here.

After six straight months of declining sales, Canada’s housing market finally showed signs of life in May. National home sales climbed 3.6 per cent month-over-month, the first gain since last November.

But before anyone calls it a comeback, let’s be honest about what the data actually says.

If this is our so-called “pent-up demand,” the market’s in no rush. In the first quarter, uncertainty around the Canadian election prevented buyers from making decisions. The industry assumed this activity would get pulled into May and June, once the election was behind us. This assumption was overestimated, albeit correct.

Yes, activity picked up. But it didn’t take off. And while buyers re-entered the ring, they were met by a wave of sellers with more speed and confidence.

Canadian Real Estate Association (CREA)’s latest report confirms what observers like me have already been signaling: new supply continues to outpace new demand, and the much-awaited rebound has landed more like a soft echo than a rally.

What’s unfolding is a quiet rebalancing, and if you’re not reading between the lines, you’re missing the most important shift we’ve seen in over a year.

A market on the move, but not in a hurry

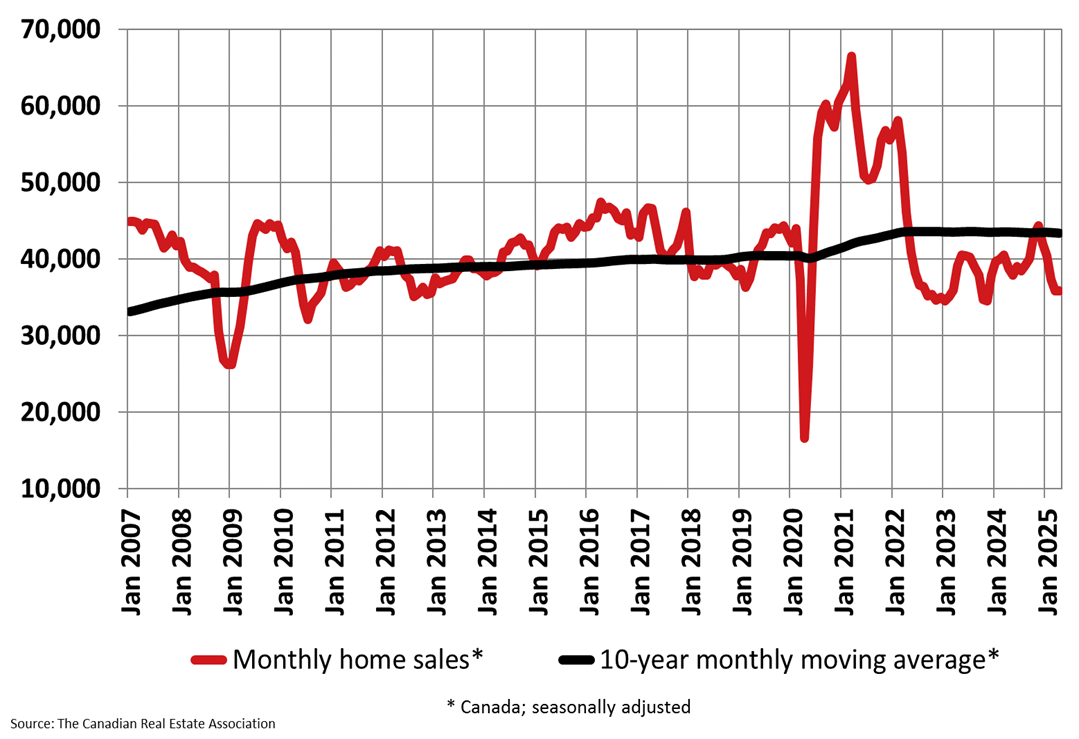

May’s 3.6 per cent sales bump was driven largely by Toronto, Calgary, and Ottawa, cities with enough volume to move the national needle. But even with that lift, overall activity remained 4.3 per cent below the same month last year. The chart below shows the sales trend from 2007 onwards.

So yes, there was movement. But not velocity.

There’s no urgency here. Buyers are still cautious. And that, in itself, is telling.

Inventory is building. Slowly, steadily, strategically.

What’s changing faster than demand is supply. New listings climbed another 3.1 per cent in May, the third straight monthly gain. At 201,880 active listings, inventory is now up 13.2 per cent year-over-year, and closing in on the long-term average.

This is a measured return of confidence from sellers who, it now feels, were sitting on the sidelines through most of 2024, and is enough to tilt the market dynamic.

The national sales-to-new listings ratio held steady at 47 per cent, well below the 10-year norm of 55 per cent. Technically, the market is balanced. Functionally, it’s beginning to lean in favour of buyers.

That’s the signal under the surface: choice is on the rise, and with it, leverage. It’s a pattern that closely resembles what’s been unfolding in the GTA, where an increase in active listings and subdued demand has given buyers significantly more negotiating power and time than they’ve had in recent memory.

Prices have leveled, but haven’t rebounded

After several months of national price declines, May brought something close to a pause. The MLS Home Price Index slipped just 0.2 per cent month-over-month, while the actual national average sale price settled at $691,299, down 1.8 per cent from May 2024.

Sellers are returning in greater numbers, as evidenced by rising inventory, but they’re still careful when it comes to pricing. Most are listing to test buyer interest, not to stretch the market.

Buyers, for their part, are starting to re-engage, but without urgency. The uptick in May sales signals renewed interest, yet not enough to create upward pressure on prices. While there are early signs that values may be stabilizing, there’s still no convincing momentum to suggest a rebound is underway.

Regionally, the picture is mixed. Ontario and British Columbia saw average prices decline by roughly 3 per cent to 4 per cent, weighing on the national average. Elsewhere in the country, average prices moved higher, with Manitoba, Quebec, Saskatchewan, and Newfoundland and Labrador posting year-over-year gains of 8 per cent to 10 per cent.

In short: the fire isn’t raging, but the market’s not frozen either. Regional conditions are now doing most of the heavy lifting.

We’ve entered a negotiation market

This is not a hot market. It’s not a correction, either. It’s something in between, which I’d like to call a negotiation market, where nothing is guaranteed, and everything is up for discussion.

And in such a market, knowledge is leverage.

Buyers have the upper hand, for now. Inventory is climbing, options are widening, and urgency is low. For the first time in years, the market is giving them space to think, to compare, and most importantly, to negotiate. But that window is finite. If rates fall later in the year, demand could pick up again, narrowing that gap.

In fact, some relief has already arrived. According to the Q1 2025 Housing Affordability Monitor from the National Bank of Canada, mortgage rates have edged down, easing the burden of ownership slightly. The national MPPI, mortgage payments as a percentage of income, dropped to 55.4 per cent, its lowest level in nearly three years.

Sellers aren’t out of options, but strategy matters more than ever. This isn’t a list-it-and-leave-it market. It rewards precision: pricing to match the moment, staging that resonates, and a narrative that justifies value.

Still a market for the measured

The market performance in May does not seem like the beginning of a boom. It’s the return of discipline.

Buyers are re-entering the arena, not in droves, but with intention. They’re more cautious, more analytical, and more willing to walk away. This time, it’s not about chasing prices. It’s about making informed moves when the terms are right. The market is offering room to negotiate, and savvy buyers are taking it.

What comes next won’t be about who moves first, but who moves smartest.

Because in this new phase of Canadian real estate, it won’t be the boldest who wins. It will be the best-informed.

Daniel Foch is the Chief Real Estate Officer at Valery.ca, and Host of Canada’s #1 real estate podcast. As co-founder of The Habistat, the onboard data science platform for TRREB & Proptx, he helped the real estate industry to become more transparent, using real-time housing market data to inform decision making for key stakeholders. With over 15 years of experience in the real estate industry, Daniel has advised a broad spectrum of real estate market participants, from 3 levels of government to some of Canada’s largest developers.

Daniel is a trusted voice in the Canadian real estate market, regularly contributing to media outlets such as The Wall Street Journal, CBC, Bloomberg, and The Globe and Mail. His expertise and balanced insights have earned him a dedicated audience of over 100,000 real estate investors across multiple social media platforms, where he shares primary research and market analysis.